Time to replace Swiss real estate with bonds?

Swiss real estate investments or bonds? No question: real estate.

Here are my reasons:

1) The return on directly held real estate is still much more attractive: the net cash flow return (the return resulting from rental income minus maintenance and renovation costs) averages 3.2% across all property categories, according to Wüest Partner. By contrast, the bond yield is 1% for government bonds and 1.5% for the Swiss Bond Index AAA-BBB. This yield difference of around 2 percentage points is very significant, see 2).

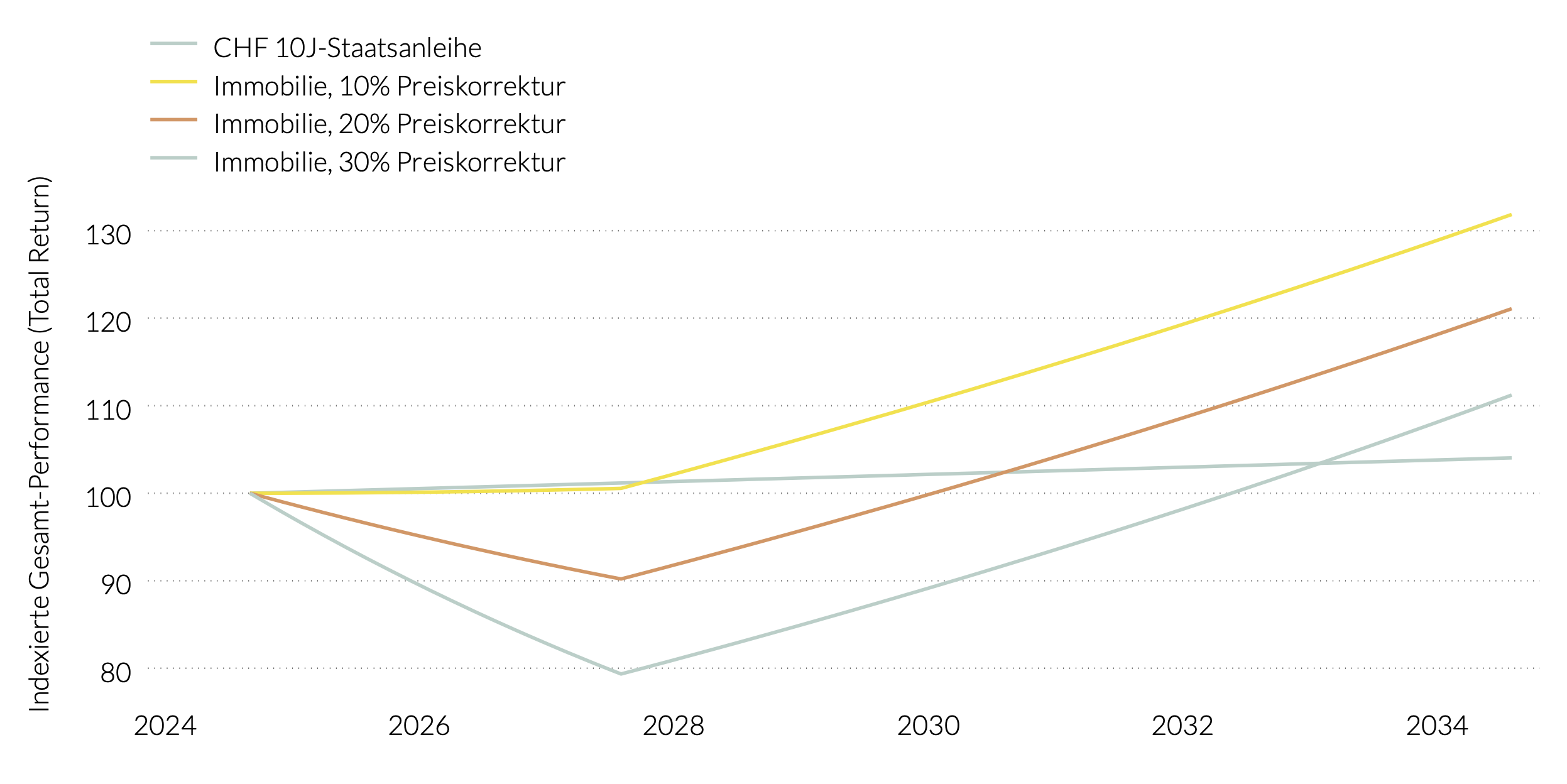

2) What if property prices fall? The higher cash flow yield from real estate can offset the loss in value over the years, as I show in the figure below. The price correction of real estate investments simulated in the figure takes place over a period of three years. After that, prices are kept constant.Even if property valuations correct by 30%, the cumulative return after 10 years is the same as an investment in a 10-year government bond. A 10% decline in valuation results in an annual return of just under 3% over 10 years, while a 20% decline in price results in an average annual return of just under 2% – twice as high as the 1% return on a 10-year government bond. Thanks to the higher cash flow return (which rises to 4.2% in my examples due to the falling denominator when the valuation declines), the slump will be made up for within a few years. In comparison, it will take 10 years to make up for last year's slump in bond prices.

Chart 1: Total return scenarios for real estate vs bonds if property prices fall by 10% / 20% / 30%

3) The correction is underway. If we could predict the future perfectly and property valuations were set to fall significantly in the coming years, it would make sense to sell property investments today and buy them back after the correction. However, it is not quite that simple. Anyone who has to sell a property today that is valued very close to market value will already have to expect a loss on the sale. Based on the prices of listed real estate funds, I estimate that a loss of 10-15% compared to the valuation would already have to be accepted today – depending on the location, of course. If a property is sold today, the loss is locked in. If the capital is used to purchase a 10-year government bond instead, this loss will not be recouped even in 10 years. If, on the other hand, the property is retained, the loss can be recouped in 4 years at the latest thanks to the higher cash flow yield.

Conclusion

Only sell your real estate investments if you expect property prices to fall significantly more than the 10-15% implied by my assessment of market valuations. And even then, in order to generate a higher return than bonds in the long term, the real estate investment must be purchased again at the right time. If the real estate investment is sold today and the money is instead invested in bonds, the return will be disappointing.

This publication is available only in German.

Write To Me

I provide advice in German, English and French.